$50k Prop Firm Account vs. $50k Personal Account

A $50k prop firm account and a $50k personal account sound like the same thing. They’re not. One gives you $50,000 of actual breathing room. The other gives you about $2,000 before the account is gone.

That difference changes everything about how you size trades, how much you can make, and whether the account is even worth trading.

The core difference

With a personal account, your drawdown is your entire balance. You have $50,000 of room to work with. You can size your trades based on a percentage of that full amount, ride out losing streaks, and recover.

With a prop firm account, your drawdown is not $50k. On most firms like Apex, TopStep, or similar, a 50k account comes with roughly a $2,000 to $2,500 maximum drawdown. That’s it. Hit that number and the account is gone.

So when you’re trading a $50k prop firm account, you’re really managing a $2,000 risk budget with access to $50k of buying power. That’s a massive difference when it comes to how much you can risk per trade and how much you can realistically make.

What this means for risk per trade

On a $50k personal account, risking 1% per trade means risking $500. That’s a standard, conservative approach. You have plenty of room to absorb a rough patch.

On a prop firm account, the math depends on which phase you’re in.

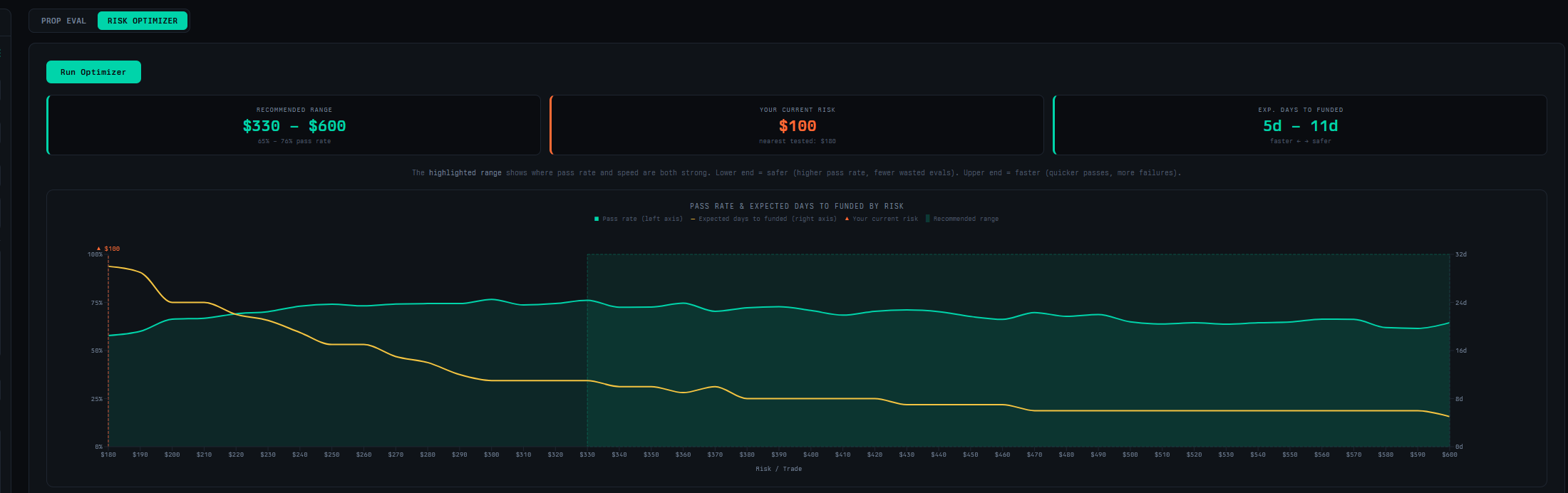

During the eval, you can actually size similarly to a personal account. The optimizer suggests a range of $330 to $600 for this edge. That’s aggressive relative to the drawdown, but it makes sense. You’re trying to hit the profit target quickly, and a failed eval only costs you the fee. You can always buy another attempt.

That said, these numbers are specific to a 50% win rate with a 1.5:1 reward-to-risk ratio. If your edge is different, especially if your win rate or profit factor is lower, the optimizer will recommend a smaller range. Always run the optimizer with your own stats before sizing your eval trades.

Once you’re funded, everything changes. Now you’re protecting a live account that’s generating real income. Blowing a funded account means losing that income stream and starting over from the eval. This is where most funded traders get into trouble. They keep sizing as if they’re still in the eval when they should be playing it much tighter.

On a funded account, optimal risk drops to around $120 to $180 per trade. That might not sound like much, but it’s what gives you the room to survive losing streaks and keep collecting payouts over time.

What you can realistically make

Let’s put some rough numbers on this.

Personal account ($50k)

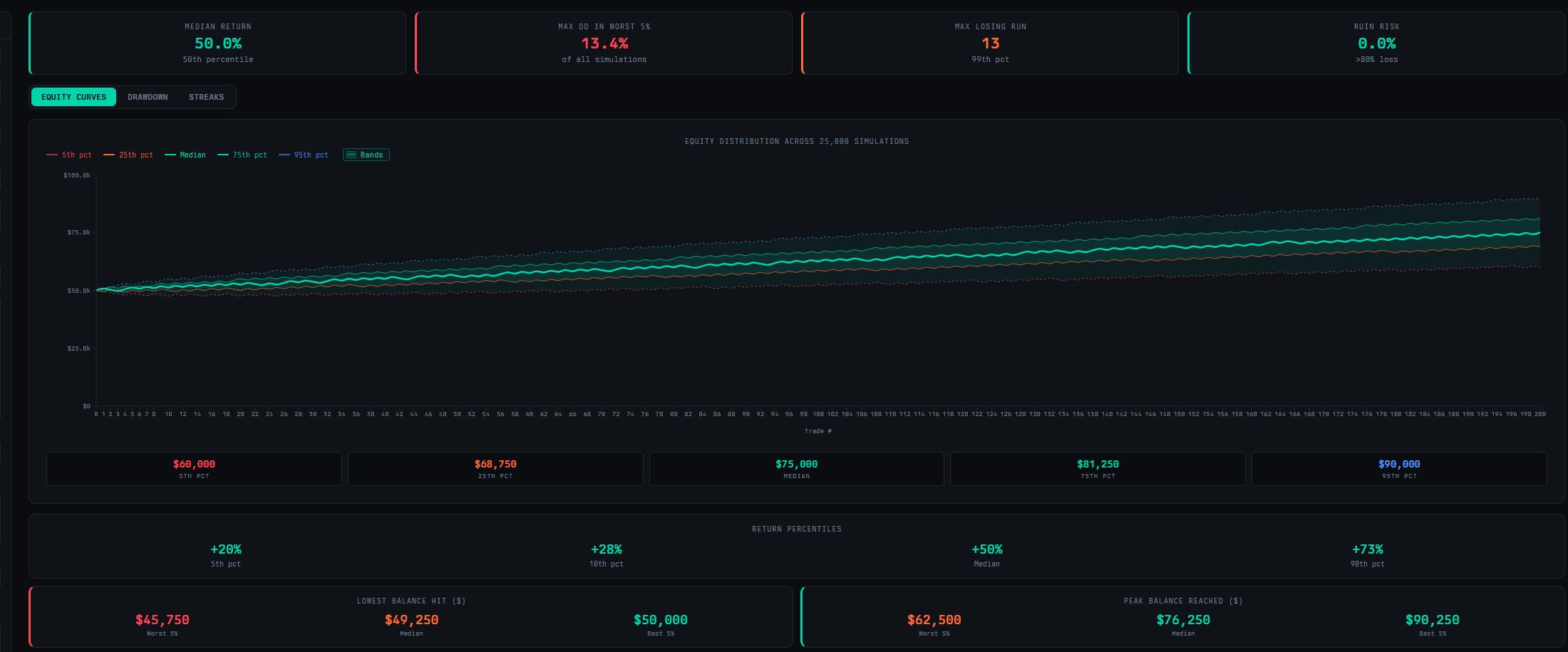

Say you have a 50% win rate with a 1.5:1 reward-to-risk ratio, risking 1% ($500) per trade, taking around 60 trades per month.

Your expectancy per trade is positive. With those numbers, winning trades pay $750 and losing trades cost $500. That works out to around $7,000 to $8,000 on a median month. Even on a rough month where variance goes against you, you’re still likely to be profitable. And you keep 100% of it.

The key thing here is that you own the account. There are no profit targets, no drawdown ceilings, no rules about consistency. You just trade your edge and let the math play out.

Prop firm account ($50k)

Same edge, but now you’re funded and sizing at $120 to $180 per trade to protect the account. Your per-trade gains are much smaller, and you only keep 80 to 90% of what you make depending on the firm’s profit split.

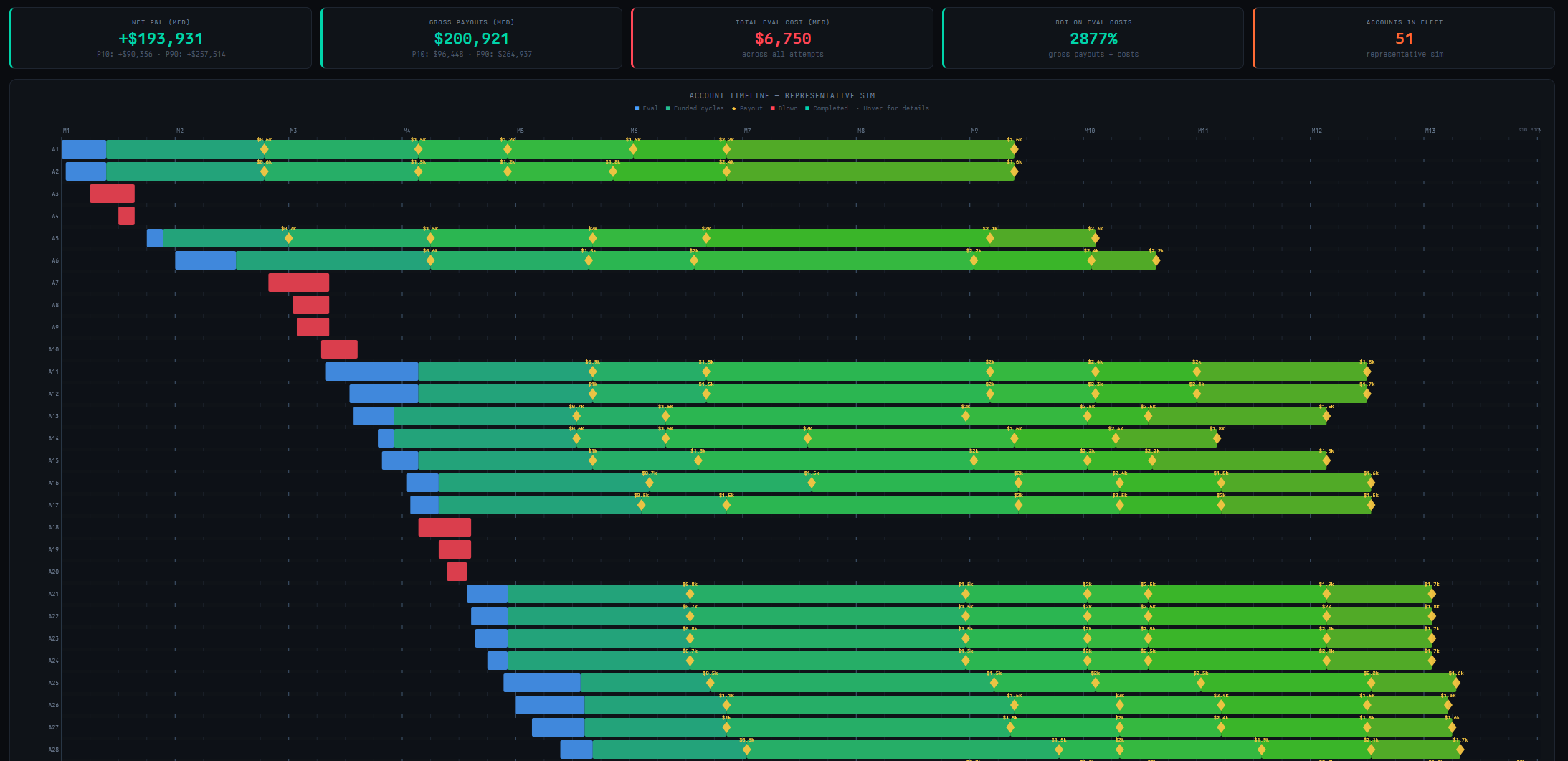

The sim models funded income in payout cycles. Your first payout takes about a month and brings in around $660. After that, subsequent cycles speed up to roughly every 23 days, with payouts growing to $1,500 to $2,500 as the account buffer builds. Over six payout cycles, the median cumulative take-home is around $11,200.

That works out to roughly $2,000 to $2,500 per month once you’re rolling. Significantly less than a personal account on a per-account basis, but the funded account cost you maybe $150 to $300 in eval fees to get. The personal account cost you $50,000 of your own money. That changes the math completely.

So which one is better?

It depends on where you are.

If you have the capital and a proven edge, a personal account is better in almost every way. No rules, no drawdown ceilings, full profits, and you can size properly. It’s not even close on a per-account basis.

If you don’t have $50k to put up, prop firms give you access to buying power you wouldn’t otherwise have. The tradeoff is that your risk budget is tiny and the rules are strict. You’re essentially paying a small fee to rent leverage with a very short leash.

The mistake most people make is comparing them as if they’re the same product. They’re not. One is an investment account. The other is closer to a leveraged performance contract.

Where the prop firm model gets interesting

The real advantage of prop firms isn’t any single account. It’s the ability to run multiples.

Running a fleet of funded accounts with the same edge changes the economics entirely. In the sim, a fleet running this edge produced a median net P&L of around $194,000 over a year, on a total eval investment of under $7,000. That’s a return on eval costs of nearly 2,900%.

Even the bottom 10% of simulations brought in over $90,000. The model works because you’re continuously replacing blown accounts with new evals, and the edge compounds across the fleet over time.

That’s the fleet model, and it’s where prop trading starts to make financial sense even for traders who could afford a personal account.

Try it yourself

The best way to see how these numbers play out for your specific edge is to run both simulations yourself.

Use the standard simulation mode to model a personal account. Then switch to Funded PA mode to model the same stats on a prop firm account. Compare the results side by side.

If you’re curious about running multiple accounts, the Fleet mode lets you model that too.

The numbers might surprise you in both directions.